Learn more how to embed presentation in WordPress

- Slides

- 6 slides

Published Mar 29, 2013 in

Business & Management

Direct Link :

Copy and paste the code below into your blog post or website

Copy URL

Embed into WordPress (learn more)

Comments

comments powered by DisqusPresentation Slides & Transcript

Presentation Slides & Transcript

PRODUCTIVITY AND INNOVATION SCHEME

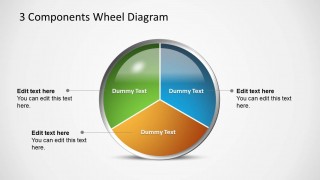

Last updated on February 19, 2013 PRODUCTIVITY AND INNOVATION SCHEME Purchase / lease of PIC Automation Equipment Includes computer, laptop, printer, fax machine, and office system software. Training of Employees Cost spent on internal Workforce Skills Qualification courses for staff222s skills upgrading. Acquisition of Intellectual Property Cost of patented technology for use in manufacturing process; Price paid for trademark and copyrights. Registration of Intellectual Property Costs incurred to register patents, trademarks, designs and plant varieties Research & Development Salaries for R&D personnel and fees to R&D institutes for activities undertaken. Approved Design Projects Fees to engage in-house qualified designers or outsourced to approved design services providers to carry out approved design activities. It pays to be productive You can get up to 400% tax deduction under PIC. Invest in any of these 6 categories to take advantage of the tax savings scheme.

Last updated on February 19, 2013 To support small and growing businesses which may be cash-constrained, to innovate and improve productivity, businesses can exercise an option to convert their expenditure into a non-taxable cash payout. They can convert up to S$100,000 (subject to a minimum of S$400) of their total expenditure in all the six qualifying activities into cash payouts. An eligible business can opt to convert 60% of qualifying PIC expenditure (capped at S$100,000) into a non-taxable cash payout, amounting to S$60,000 per YA. Claimable any time after the end of each financial quarter, but no later than the due date for the filing of its income tax returns for the relevant year. Businesses may obtain the first quarterly cash payout starting July 2012. Businesses that can opt for the cash payout are sole-proprietorships, partnerships, companies (including registered business trusts) that have: Eligibility criteria

Last updated on February 19, 2013 Qualifying activities Brief description of qualifying expenditures under the PIC Total deductions/allowances under the PIC (as a % of qualifying expenditure) Acquisition or Leasing of Prescribed Automation Equipment Costs incurred to acquire/lease prescribed automation equipment 400% allowance or deduction for qualifying expenditure subject to the expenditure cap, 100% allowance or deduction for the balance expenditure exceeding the cap Training Expenditure Costs incurred on: In-house training (i.e. Singapore Workforce Development Agency (223WDA224) certified, Institute of Technical Education (223ITE224) certified; or All external training. Acquisition of Intellectual Property Rights (223IPRs224) Costs incurred to acquire IPRs for use in a trade or business (exclude EDB approved IPRs and IPRs relating to media and digital entertainment contents) Registration of Intellectual Property Rights (223IPRs224) Costs incurred to register patents, trademarks, designs and plant variety Design Expenditure Costs incurred to create new products and industrial designs where the activities are primarily done in Singapore Research & Development (223R&D224) Costs incurred on staff, costs and consumables for qualifying R&D activities carried out in Singapore or overseas, if the R&D done overseas is related to the taxpayer222s Singapore trade or business 400% tax deduction for qualifying expenditure subject to the expenditure cap*. For qualifying expenditure exceeding the cap for R&D done in Singapore, deduction will be 150%. For balance of all other expenses, including expenses for R&D done overseas, deduction will be 100% Notes: Total expenditure cap for YA 2011 and YA 2012 - $800,000 for each of the six qualifying activities. Total expenditure cap for YA 2013 to YA 2015 - $1,200,000 for each of the six qualifying activities. The Productivity and Innovation Credit (PIC) Scheme has been further enhanced for Singapore Budget 2011. It is a scheme to provide tax incentives so as to encourage businesses to invest and upgrade along the innovation value chain. The table below outlines the benefits of the PIC: Expenditure S$100,000 S$100,000Deduc037ons S$100,000 S$400,000TAX SAVINGS S$17,000 S$68,000Be fo re PIC: 037036035035 034033032031 030027 026025036024023033034024024034024026022021033026032030020023022021031031030026017034017036022032026032016034023035026 034r 020034033024034024026021032026 022f024032026023013034013026nttb026021024026020021035032026f007026032016034026006034033034035 021031026032 021r026035 034006023005034013026 004021 r026024021 003023033006024026002026001ntt027ttt026r026n201b A036 er PIC: 215036024023033034024024034024026022021033026033f217026034033220f030026235ttb026017034017036022240f033026f033026032016034026022f024 032026f007026 032016034026024021005034026034 r020034033017023032036035 034013 004021 r026024021 003023033006024026002026001235tt027ttt026r026n201b

Last updated on February 19, 2013 Estimated Taxable Income Estimated Tax Payable Effective Tax Rate Total Qualifying Expenditure (Combined limit of all Six Activities for Total PIC Claim Effective Tax Payable (after PIC claim) 100,000 8,075 8.10% 25,000 100,000 0 200,000 16,575 8.30% 50,000 200,000 0 300,000 25,075 8.40% 75,000 300,000 0 400,000 42,075 10.50% 100,000 400,000 0 500,000 59,075 11.80% 125,000 500,000 0 600,000 76,075 12.70% 150,000 600,000 0 700,000 93,075 13.30% 175,000 700,000 0 800,000 110,075 13.80% 200,000 800,000 0 900,000 127,075 14.10% 225,000 900,000 0 1,000,000 144,075 14.40% 250,000 1,000,000 0 2,000,000 314,075 15.70% 500,000 2,000,000 0 3,000,000 484,075 16.10% 750,000 3,000,000 0 4,000,000 654,075 16.40% 1,000,000 4,000,000 0 5,000,000 824,075 16.50% 1,250,000 5,000,000 0 6,000,000 994,075 16.60% 1,500,000 6,000,000 0 7,000,000 1,164,075 16.60% 1,750,000 7,000,000 0 8,000,000 1,334,075 16.70% 2,000,000 8,000,000 0 9,000,000 1,504,075 16.70% 2,250,000 9,000,000 0 9,600,000 1,606,075 16.70% 2,400,000 9,600,000 0 11,000,000 1,844,075 16.76% 2,750,000 11,000,000 0 12,000,000 2,014,075 16.78% 3,000,000 12,000,000 0 13,000,000 2,184,075 16.80% 3,250,000 13,000,000 0 14,000,000 2,354,075 16.81% 3,500,000 14,000,000 0 15,000,000 2,524,075 16.83% 3,750,000 15,000,000 0 16,000,000 2,694,075 16.84% 4,000,000 16,000,000 0 17,000,000 2,864,075 16.85% 4,250,000 17,000,000 0 18,000,000 3,034,075 16.86% 4,500,000 18,000,000 0 19,000,000 3,204,075 16.86% 4,750,000 19,000,000 0 20,000,000 3,374,075 16.87% 5,000,000 20,000,000 0 21,000,000 3,544,075 16.88% 5,250,000 21,000,000 0 22,000,000 3,714,075 16.88% 5,500,000 22,000,000 0 23,000,000 3,884,075 16.89% 5,750,000 23,000,000 0 24,000,000 4,054,075 16.89% 6,000,000 24,000,000 0 25,000,000 4,224,075 16.90% 6,250,000 25,000,000 0 26,000,000 4,394,075 16.90% 6,500,000 26,000,000 0 27,000,000 4,564,075 16.90% 6,750,000 27,000,000 0 28,000,000 4,734,075 16.91% 7,000,000 28,000,000 0 28,800,000 4,870,075 16.91% 7,200,000 28,800,000 0

RIKVIN PTE LTD 20 Cecil Street, #14-01, Equity Plaza, Singapore 049705 Main Line : (+65) 6320 1888 Fax : (+65) 6438 2436 Email : info@rikvin.com Website : www.rikvin.com Reg No 200100602K EA License No 11C3030 This material has been prepared by Rikvin for the exclusive use of the party to whom Rikvin delivers this material. This material is for informational purposes only and has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. Where the source of information is obtained from third parties, Rikvin is not responsible for, and does not accept any liability over the content. Helpful Links: Company Registration Singapore Work Visas Business Services Accounting Services Offshore Company

More Presentations

By singaporerikvin

Published Mar 27, 2013

By singaporerikvin

Published Mar 28, 2013

By singaporerikvin

Published Mar 29, 2013

By singaporerikvin

Published Mar 30, 2013

By singaporerikvin

Published Mar 31, 2013

By singaporerikvin

Published Apr 1, 2013